No Fees for Life IRA

At Patriot Gold Group, we have more than 50 years of experience being an industry leader in the field of precious metal investments. If you're looking for ways to invest your precious metals, consider opening a precious metals IRA. Our experts can help you find investment opportunities including a no fees for life IRA account.

Benefits of a No Fees IRA Account

Opening a precious metals IRA account is a great way to diversify your investment portfolio. With this kind of diversification, your wealth will be better protected against future market crashes. Gold and silver also offer protection against the dollar and its decreasing value while also hedging against inflation. Gold, silver, and other precious metals have been proven to increase their value as time increases.

Another benefit of precious metals investments is their continued ability to outperform traditional stocks. If you're looking to open a reliable, no fees for life IRA account, invest in precious metals today. This option will balance your portfolio and safeguard you against future threats.

To get started on opening your no fees IRA account, call the Patriot Gold Group at (877) 711-6641 or fill out the form at the bottom of this page. We look forward to helping you with your future investments.

OPEN A PRECIOUS METALS IRA IN

3 EASY STEPS

OUR NO FEE FOR LIFE IRA PROGRAM STARTS HERE. (Minimum Account Required)

Contact Our Experts

Fill out the form to get your free Gold IRA Investor Guide and speak with one of our representatives.

Transfer or Roll Over

Our 401(k) and IRA Rollover department will guide you step by step through the tax-free transfer process.

Own Precious Metals

Once your Self Directed IRA account is funded, we will help you buy and store your precious metals.

AND ENJOY ALL THE BENEFITS OF OWNING GOLD

|

|

|

|

PRECIOUS METALS IRA

Americans are facing a weakening dollar, nuclear threats from North Korea, and natural disasters at a time when lightning fast communications turn geopolitical murmurs into financial shocks. Physical gold and silver offer investors the protection of a balanced investment portfolio. Hold your metals in a self-directed Precious Metals IRA. Profits are tax-deferred when the proceeds from the sale remain with your custodian for reinvestment or are transferred to another IRA.

This Is the Riskiest Stock Market of the Past 100 Years

What if you knew that over the course of 2020, a pandemic would shut down much of the global economy – creating the steepest economic contraction since the Great Depression...

Thousands of restaurants and other businesses would close their doors – leaving millions of Americans unemployed and desperate...

Violent protests would occur in dozens of American towns and cities...

The stock market would hit a new all-time high in late February only to plunge 34% in about one month...

The U.S. Federal Reserve would cut interest rates effectively to zero and print roughly $3 trillion to support the economy and the financial system...

And Congress would sign off on an unprecedented $2 trillion stimulus package – mailing personal checks directly to people's homes.

Assuming you knew all this one year ago, what would have been your guess for the performance of various asset prices this year?

Probably nothing like what we got.

Today, the U.S. stock market is more expensive – and therefore riskier – than at any time in the past century. You must understand that risk... because last year's roller coaster ride isn't over yet...

The stock market soared 68% off its March bottom last year. Would you have thought new all-time highs were even a remote possibility after that precipitous drop?

Would you have thought that despite a raging pandemic, political upheaval, and civil unrest, stocks would surge to their most expensive valuation in history – even more expensive than the 1929 and 2000 market tops?

I've occasionally said that a wider range of outcomes for the price of a given asset indicates higher risk. For example, there's a much wider range of outcomes for small-cap mining stocks (which can soar hundreds, even thousands of percent – or collapse entirely) than for Treasury bonds (which pay 1% a year for 10-year bonds today).

The stock market has made higher highs since I got bearish in 2017... But it has also made lower lows. In other words, a wide range of outcomes occurred.

The more expensive stocks become, the riskier they are to own. And that's what we're seeing today...

The best two metrics to demonstrate how expensive stocks are today are the S&P 500 price-to-sales (P/S) ratio and the ratio of total U.S. market cap to U.S. gross domestic product ("GDP").

Over the past century or so, whenever the P/S ratio has been high, the market has tended to perform poorly, sometimes for many years. At the peak of the dot-com bubble in March 2000, the P/S ratio was 2.3. Today, it's about 2.7.

The total market-cap-to-GDP ratio was pioneered by value guru Benjamin Graham and often cited by his prized pupil, Warren Buffett. It, too, has never been as high as it is today. It peaked at 140% in 2000 and 105% in 2007. Now it's 188%.

I also follow the stock market valuation work of economist and asset manager John Hussman of HussmanFunds.com. He tracks five metrics, including the P/S ratio, that have all correlated negatively over the past century with subsequent 10- and 12-year S&P 500 performance. Roughly 90% of the time when they've been high, the S&P 500 has performed poorly for a decade.

In a recent market comment, Hussman wrote...

“Presently, I expect that the completion of this market cycle is likely to involve a loss in the S&P 500 on the order of 65-70%. I realize, of course, that this sounds insane. The problem is that this projection is fully in line with a century of evidence and is consistent with the extent of market losses that would be run-of-the-mill given present valuation extremes.”

Hussman estimates that a portfolio of 60% S&P 500 stocks, 30% long-term Treasury bonds, and 10% Treasury bills will lose 1.7% per year for the next 12 years. He estimates the S&P 500 by itself will lose 3.6% per year for the next 12 years.

Asset manager Jeremy Grantham's firm, GMO, has studied a couple dozen asset bubbles throughout history. It also publishes seven-year return forecasts for various asset classes. Grantham recently called the current market a "'real McCoy' bubble" and added, "It's truly crazy."

With stocks more overvalued than at any time in the past century, it's time to plan accordingly. Risk is high today... And we'll likely see years of underperformance when this bull market ends.

Fund Managers Provide No Added Value

So if the banks are taking such enormous percentages of your retirement savings, are they bringing you any value in return? Well, the banks would love you to believe that their expert financial management is making you a bundle. But guess what? All the scientific evidence shows that mutual funds underperform the stock market!

Year after year, in bull and bear markets, actively-managed mutual funds fail to beat index funds. So the banks are taking a huge chunk of your retirement savings and providing no value in return! And even “lower-cost” index funds end up costing you a QUARTER of your retirement savings – not so “low-cost” after all.

The Only Zero-Fee Retirement Account

So the facts are clear: retirement plans were not created for OUR benefit; they were created for the benefit of BANKS. Meanwhile, for over 5,000 years we’ve had a retirement vehicle – Gold & Silver – where your gains are truly YOUR gains. No management fees. No hidden bank fees. No fine print.

Gold & silver have outlasted every paper currency on the earth and have greatly outperformed the stock market for decades. What’s more, physical gold & silver cannot be instantly seized with the stroke of a keyboard like every financial product the banks have to offer. So convert your savings & retirement into gold & silver now, and keep the greedy banks out of your hard-earned life savings.

Big Corporations Shift the Retirement Burden to Employees

In 1990, 42 percent of employees had a pension — a guarantee by your employer that you got a good percentage of your salary & benefits upon retirement. Then the big corporate executives complained they couldn’t afford pensions anymore, so they cut pensions for a huge percentage of employees. Meanwhile, since the late 70s, those same corporate executives increased their compensation 1000% compared to 11% for their employees! (I guess we know where the pension savings went).

In short order, the corporations stopped providing pensions and shifted the burden to employees by setting up market-based retirement plans. Some of these plans, like the 401(k), were originally a corporate tax dodge for high earners and were never intended to apply to the rest of us. But big brokerages & banks saw an opportunity to expand their business, so they promoted these retirement accounts as a win for everyone. In truth, they were only a win for the corporations & banks!

Big Banks Gobble Up Your Gains

Over the past couple of decades, Americans handed over more than $10 trillion of our retirement money to the financial services industry. And the banks gobbled up a huge portion of it for themselves. The average actively-managed fund carries an annual expense of 1.3 percent. Many funds charge a fee of 2 to 3 percent – regardless of whether they earn you any money!

These percentages might sound small. But when you factor in compounding interest, the management fees on retirement accounts are ENORMOUS. In fact, you end up paying a HUGE percentage of your retirement savings to the bank. How much? Just take a look at the following numbers:

- Let’s assume an 8% annual return for all investments over a 30-year period.

- In the first scenario, you invest in gold, where there are ZERO management fees.

- In the second scenario, you invest in a bank-managed retirement account, where the fees range from 2-3%.

If you invested $100,000 in gold, after 30 years you would have…

$1,006,266. Yes, over $1 million in gold.

But if you invested $100,000 in a retirement fund, the fees alone would destroy a huge percentage of your retirement savings. After 30 years you would have…

$574,349 with 2% management fees (the bank takes 43%)

$432,194 with 3% management fees (the bank takes 57%)

The numbers don’t lie. The big banks easily pocket 50% or more of your retirement savings! In fact, the average American household will pay nearly $155,000 over the course of a lifetime in fees alone. Think about it, do you really want to invest in a system where you put up 100% of the capital, you take 100% of the risk, and you get a paltry 30% of the return? That’s quite a steal for the big banks.

The Big Banks Pocket More Than 50% of Your Retirement Investments

These percentages might sound small. But when you factor in compounding interest, the management fees on retirement accounts are ENORMOUS. In fact, you end up paying a HUGE percentage of your retirement savings to the bank. How much? Just take a look at the following numbers:

- Let’s assume an 8% annual return for all investments over a 30-year period.

- In the first scenario, you invest in gold, where there are ZERO management fees.

- In the second scenario, you invest in a bank-managed retirement account, where the fees range from 2-3%.

If you invested $100,000 in gold, after 30 years you would have…

$1,006,266. Yes, over $1 million in gold.

But if you invested $100,000 in a retirement fund, the fees alone would destroy a huge percentage of your retirement savings. After 30 years you would have…

$574,349 with 2% management fees (the bank takes 43%)

$432,194 with 3% management fees (the bank takes 57%)

For decades the banks & politicians have sold us a bill of goods about socking money away in bank-managed retirement funds. We were promised a lifetime of growth that would set us up comfortably in retirement. But even after years of record Fed stimulus that artificially propped up the stock market and padded retirement accounts, the dirty secret of bank-managed retirement funds is finally coming to light: banks are pocketing a staggering percentage of your retirement investments! In many cases, you are surrendering 50% or more of your retirement savings to the banks for the “privilege” of having them control your money. Fortunately, there’s still ONE investment option that allows you to keep 100% of your retirement savings.

We are locked into a system designed to fail

Even John Bogle, founder and former chief executive of The Vanguard Group, says the retirement options offered by financial institutions are fiction — what he called a “train wreck” in his appearance on Frontline.

IRAs and 401(k)s weren’t designed to be retirement plans but savings or thrift plans. And the returns are small: After adjusting for inflation and subtracting taxes and fees, “you’re down into a pretty paltry return, 1 or 2%,” according to Frontline, which Bogle confirms. “We don’t tell people that, you see, in this business,” Bogle adds.

|

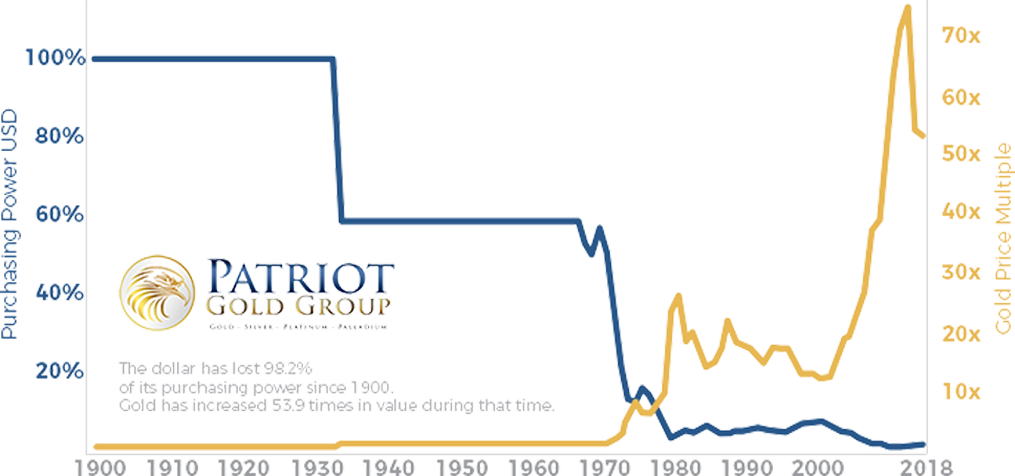

HEDGE YOUR PURCHASING POWERThe dollar has lost 98.2% of its purchasing power since 1900 while gold has increased 53.9 times in value during that same time period. In 2017, the dollar performed dismally against the 19 most-traded currencies in the world including a 12% decline against the Euro. Gold has dramatically offset the loss in purchasing power of the U.S dollar.

|

Get The Leading Gold

IRA Investor Guide

GET THE LEADING GOLD IRA INVESTORGUIDE FROM CONSUMER AFFAIRS TOPRATED GOLD IRA DEALER IN 2016 AND 2017

- What is a physical gold IRA?

- Does a physical gold IRA make sense for you?

- How do you buy a physical gold IRA?

- How do you store your physical gold?

- What are the benefits of gold IRA investment?

- What are the types of gold IRA investment?

- What causes gold prices to rise?

|

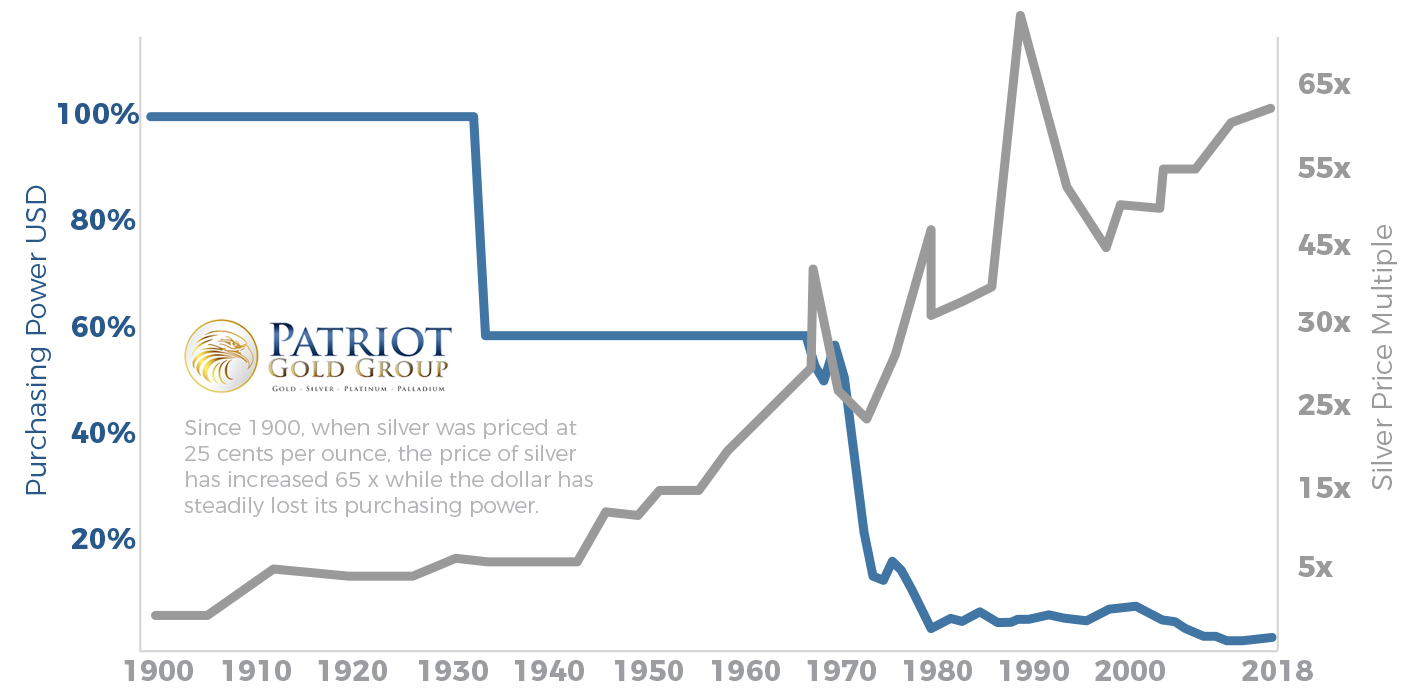

HEDGE YOUR PURCHASING POWERThe dollar has lost 98.2% of its purchasing power since 1900 while silver has increased 64.44 times in value during that same time period. In 2017, the dollar performed dismally against the 19 most-traded currencies including a 12% decline against the Euro. Smart investors have used silver to offset the loss in purchasing power of the U.S dollar. |

GET THE LEADING SILVER

IRA INVESTOR GUIDE

GET THE LEADING SILVER IRA INVESTORGUIDE FROM CONSUMER AFFAIRS TOPRATED SILVER IRA DEALER IN 2016 AND 2017

- What is a physical silver IRA?

- Does a physical silver IRA make sense for you?

- How do you buy a physical silver IRA?

- How do you store your physical silver?

- What are the benefits of silver IRA investment?

- What are the types of silver IRA investment?

- What causes silver prices to rise?

ENJOY ALL THE BENEFITS OF

OWNING GOLD AND SILVER

Control

Hold physical gold tax deferred in a Private Storage IRA or in your own hands.

Freedom

Grow your wealth in a few hours a month with your gold and silver IRA investment.

Growth

Since 1900, gold has increased in value 53.9 times while the dollar has lost 98.2%.

Security

Gold insures you against weak-performing assets and builds a balanced portfolio.

|

|

|